Share this article

Moody's recent downgrade of the U.S. credit rating marks an official end to the country’s top-tier debt status. Following Fitch's downgrade in 2023 and Standard & Poor's move in 2011, Moody's decision to lower the rating from Aaa to Aa1 underscores growing concerns about the nation's fiscal trajectory. This decision comes as Congress debates a new budget bill that could increase annual deficits, highlighting the gap between tax cuts and fiscal sustainability. Amid this debt, deficit, and political uncertainty, many investors may wonder what this means for their financial plans.

Budget Negotiations Have Historically Created Periods of Uncertainty

Budget negotiations and debt ceiling standoffs have created significant market volatility over the past fifteen years. There have been many examples, including the 2011 downgrade of the U.S. debt by Standard & Poor's, the fiscal cliff in 2013, the government shutdown of 2018 and 2019, and more. However, in all cases, agreements were eventually reached, allowing markets to stabilize and advance once more.

Even after the 2011 downgrade, which was unprecedented at the time and resulted in a market correction, the S&P 500 experienced a full recovery within months. It may seem paradoxical, but despite these downgrades, U.S. Treasury securities are still considered a safe-haven asset during times of market volatility and continue to serve as an important foundation for financial markets.

So, when it comes to the national debt and Washington budget battles, it's important to keep the issues in perspective. As taxpayers, voters, and citizens, it’s natural to be concerned that the country is not on a sustainable fiscal path. Unfortunately, there are no easy solutions to these challenges, and various commissions and proposals have failed to truly reduce the size of annual budget deficits.

As significant as these issues are, it’s also important to avoid overreacting with our investment portfolios. While past fiscal challenges and downgrades have led to uncertainty, markets have historically recovered and stabilized over time. A disciplined investment approach focused on long-term goals, diversification, and investment fundamentals – rather than on Washington headlines or hope that Congress will solve the deficit problem – is still the best way to achieve long-term goals.

The downgrade by Moody’s comes at a critical moment as investors shift their attention from tariffs to Washington's budget proposal. While markets performed well following last year’s presidential election partly on expectations of pro-growth policies and an extension of the Tax Cuts and Jobs Act of 2017 (TCJA), the Moody's announcement serves as a reminder of the other side of the fiscal situation.

Specifically, Moody's emphasized that “successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs,” and that they “do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.”

Tax Cuts and Jobs Act Provisions Are on Track to Be Extended or Made Permanent

Perhaps not coincidentally, Congress is in the middle of crafting a new budget bill, and some provisions are still evolving. The latest proposal aims to provide certainty by extending the individual tax cuts from the TCJA, which would otherwise expire at the end of 2025. This would avoid a potential "tax cliff" – a scenario where tax rates would revert to pre-TCJA levels, potentially creating economic disruption. By addressing these concerns well in advance of the expiration, policymakers hope to provide stability for both consumers and businesses.

The comprehensive tax package contains numerous provisions affecting both businesses and individuals. Key elements which are subject to change include:

For Individuals:

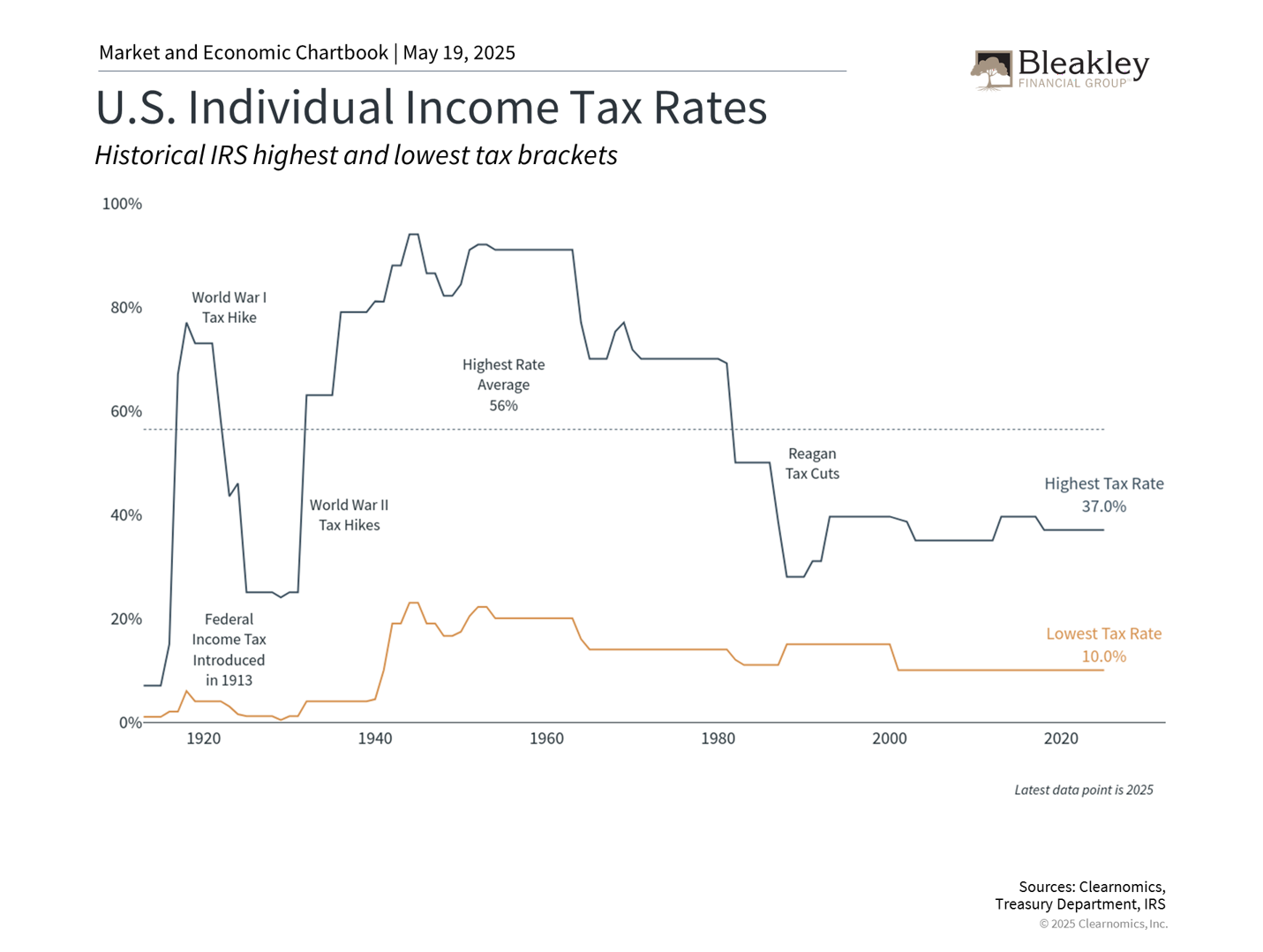

- The TCJA individual tax rates would become permanent, with a top rate of 37%

- The child tax credit would increase from $2,000 to $2,500 through 2028

- The state and local tax (SALT) deduction cap is a point of controversy, with some proposing a $30,000 cap (an increase from the current $10,000)

- Tips and overtime pay would be exempt from income tax through 2028

- Interest on auto loans would become tax-deductible through 2028

- A new type of savings account known as the “money account for growth and advancement” (referred to as “MAGA accounts”) would be created for children under 8 for education, small business investments, and first-home purchases

For Businesses:

- The pass-through business deduction would increase from 20% to 23% and become permanent

- 100% bonus depreciation for qualified business assets would be reinstated for property acquired between January 2025 and 2029

- Research and development tax deductions would be reinstated

Notably absent from the proposal are provisions for a “millionaire tax” and changes to carried interest tax treatment, which some had anticipated. The debt ceiling, which represents how much the country can borrow, could also be raised by $4 trillion.

Deficits May Continue to Add to the Debt

While the latest proposal includes approximately $1.6 trillion in spending reductions through changes to programs like Medicaid and nutrition assistance, they are outweighed by tax cuts and spending increases in other areas.

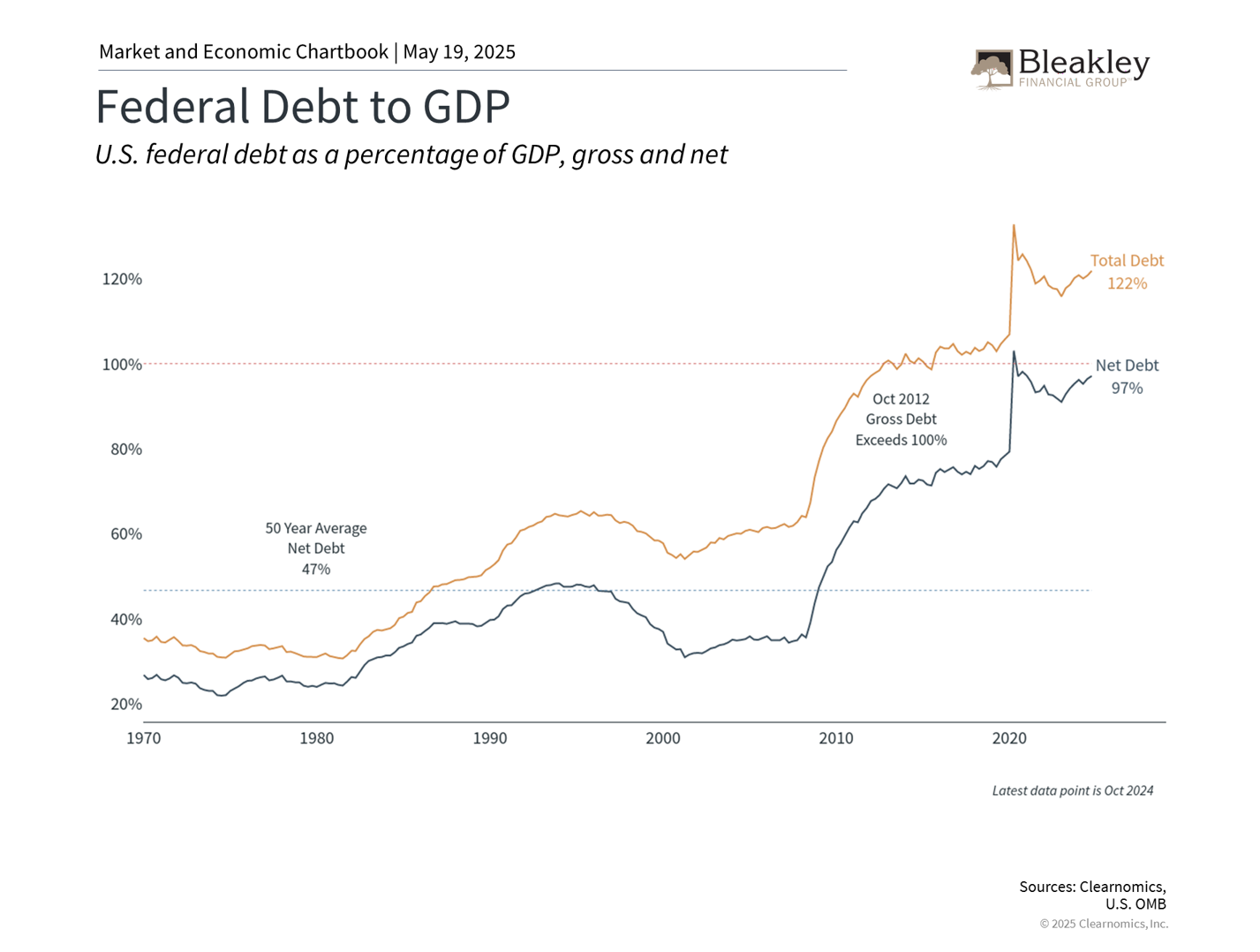

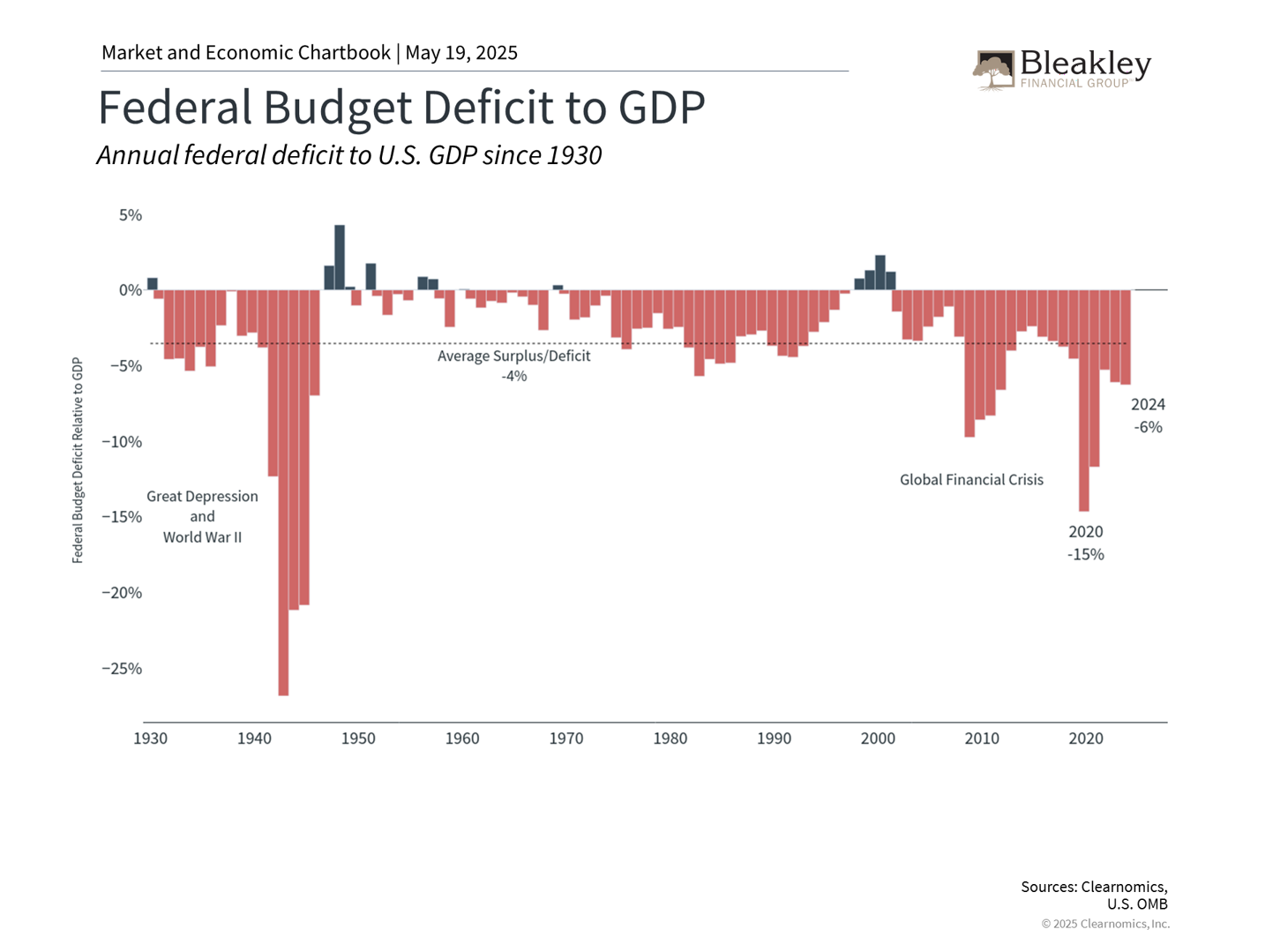

Annual budget deficits matter because they add to the national debt, which already exceeds $36 trillion, or about $106,000 per American. It’s reported that the proposed budget could add an estimated $3 trillion or more to the debt over the next ten years. The most recent estimate by the Joint Committee on Taxation, a nonpartisan committee of Congress, showed that the debt could increase by $3.7 trillion over this period.

It’s no secret that the national debt has grown considerably in recent decades, with interest payments continuing to rise. Given that most federal spending is allocated toward mandatory programs like Social Security and Medicare, it’s politically difficult to agree on significant spending cuts. This is why some worry that tax rates will eventually need to rise to make up the difference, even though the TCJA may be extended or made permanent in the near term.

Although the deficit and debt levels are important considerations for the long-term health of the economy, their immediate impact should be kept in perspective. Markets have historically performed well across varying levels of government debt and deficit spending. Ironically, some of the strongest market returns over the past two decades have occurred after the worst deficits, since these usually coincided with economic crises when markets were at their lows. In other words, making investment decisions based on government spending and deficits would have been counterproductive.

The bottom line? A downgraded U.S. credit rating highlights concerns over the country’s long-term fiscal trajectory. The current budget battle could further add to these issues. Nevertheless, history suggests that the best way for investors to navigate these challenges is by staying invested and maintaining a long-term financial plan.

- Article published on 5/19/25 -

BFG 25-0102

Disclaimer

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

This commentary is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Bleakley Financial Group, LLC does not guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward-looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

About the Author