Share this article

Investors and the financial media tend to focus on macroeconomic concerns such as inflation, labor markets, and the Fed. While these topics are important, history shows that the economy and markets grow over long periods of time due to technological innovation and gains in productivity. It’s for this reason that recent developments in artificial intelligence have captured the attention of investors and economists. They have also led to disagreements about the short-term investment opportunities across technology stocks and, more importantly, about the long-term effects on the economy, productivity and the labor market. What impact do new technologies tend to have on markets and investor portfolios?

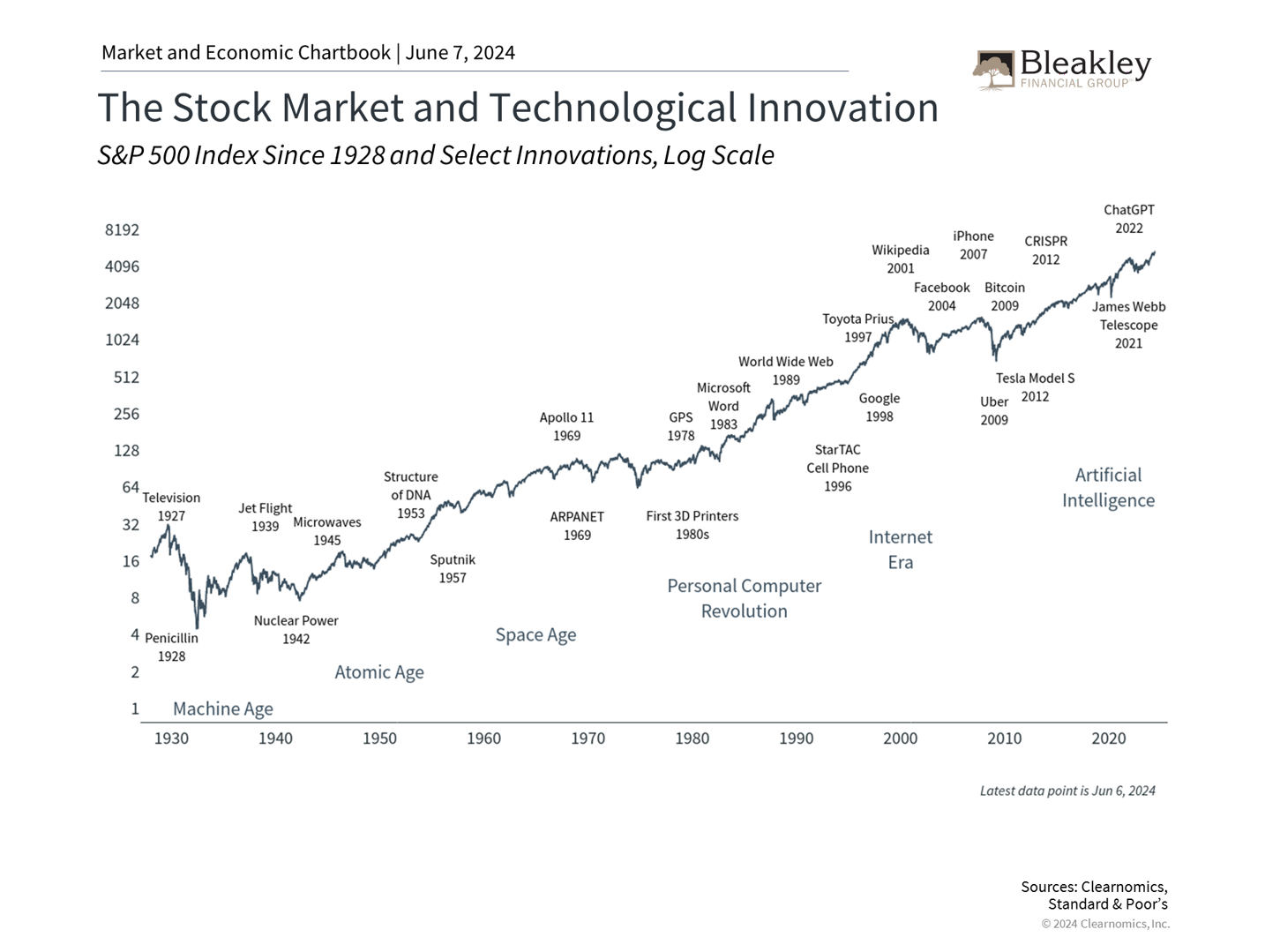

Innovation Supports Market and Economic Growth Over Time

It’s understandable that investors often focus on the financing side of markets and the economy, including topics such as interest rates and Fed policy. Projects in the real world need funding so the purpose of the financial system is to direct capital toward its highest-value use. In doing so, investors hope to generate positive returns that grow their capital and be deployed to new activities. When done well, this can create a virtuous cycle that leads to long run economic growth.

The key, however, is for these investments and their returns to correspond to true innovation. As the accompanying chart shows, the past century has been one of unceasing technological advancement from the first assembly lines to putting a man on the moon, to the entire world being connected on a single information network. In fact, the modern era is driven by the idea that technology should improve every year, whether it’s our cell phones, computers, cars or thermostats. In turn, the services they enable should also improve the quality of our lives, including ordering food delivery, watching movies on demand, communicating with friends and family, better medical care, and making investment decisions. Of course, this does not always play out as expected, such as with concerns over social media.

What makes the information age unlike previous periods in history? Unlike physical objects such as buildings, machines on factory floors, or hardcover books, one person's use of a digital service doesn't prevent another from using it. This is important because digital tools allow knowledge workers to be more productive in a scalable way, creating benefits across a variety of industries and scientific fields. Knowledge workers are also expensive and time-consuming to train, so even small gains in productivity can compound over time.

These are all reasons why many believe that AI is the pinnacle of the information age. Today's optimism on AI stems from the idea that it could enable even more technological innovations and accelerate productivity further. So far, examples of AI-boosted productivity in the business world have mainly been in the form of generating content, automating tasks, and analyzing data. It's hard to predict exactly what impact AI will eventually have, partly due to the pace of advancement, and partly because the impact of new technologies is simply hard to imagine. What's clear from the chart above is that the stock market did not move up in a straight line with past innovations, and many of their effects took years to materialize.

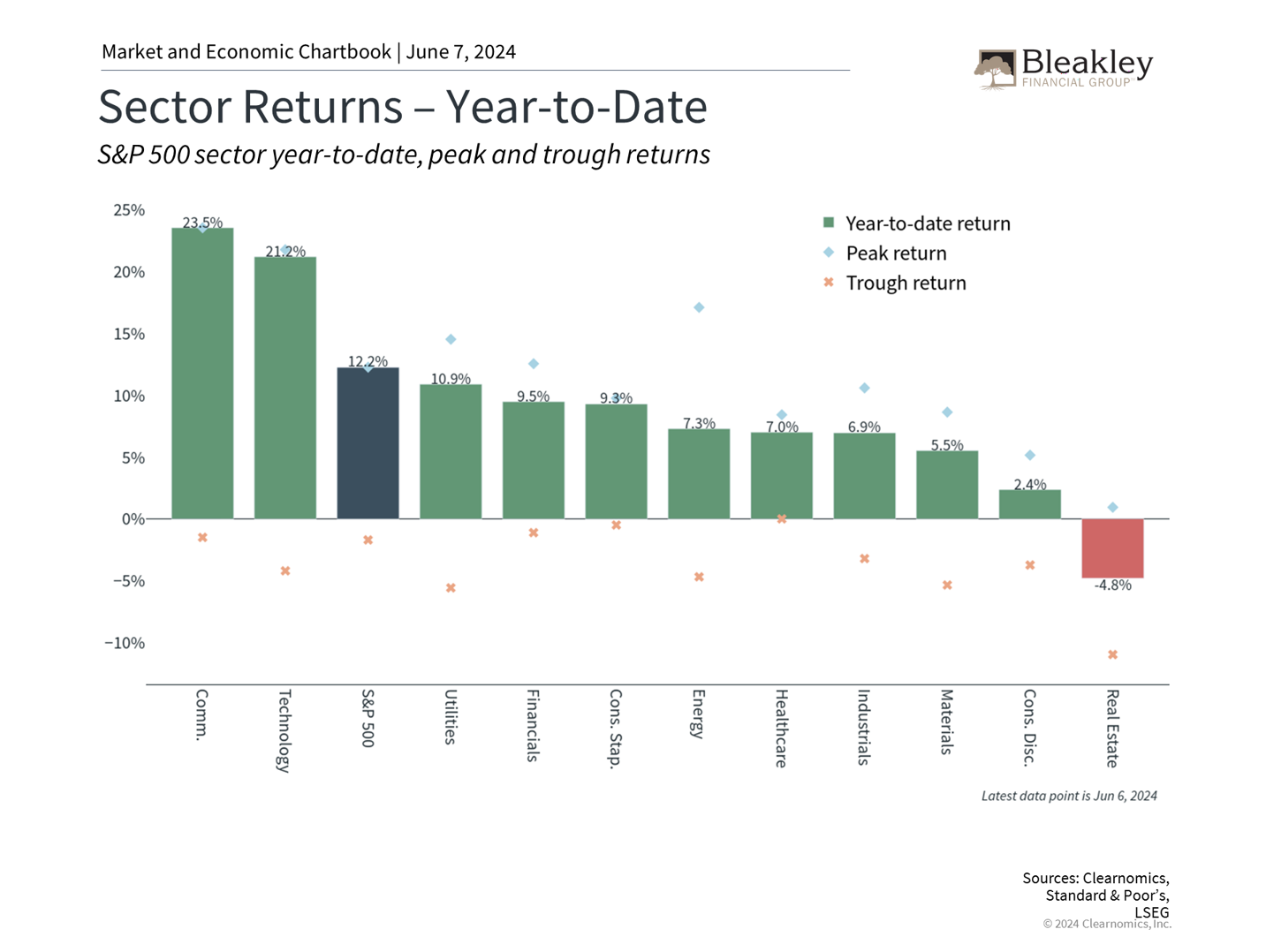

AI Stocks Have Outperformed but Other Sectors Are Benefiting Too

As computer scientist Roy Amara said, investors tend to overestimate the impact of technology in the short-term and underestimate the effect in the long run. There are many examples of this throughout history, most recently with the dot-com boom and bust. In the late 1990s and early 2000s, many companies rushed to add .com and .net to their names, capitalizing on the demand for all things internet related. This also occurred during the “tronics boom” of the early 1960s when a wave of companies with that suffix in their names benefited from investor exuberance for the consumer and business adoption of electronics.

While these trends generated significant returns for many years, the bubbles eventually burst. In hindsight, investor capital was clearly not put to its best use despite the promises of outsized returns. The challenge is knowing if there is a bubble to begin with. Today, some are rebranding themselves as AI companies, updating their websites, and using .ai domain names - no different than in the 1990s and 1960s. The performance of large cap stocks has been driven by a handful of companies related to technology and AI, including the Magnificent 7. Companies like Nvidia, for instance, have become household names when only a couple years ago they were primarily known for video game graphics cards.

There are clear differences between today's market and the dot-com bubble, the most important being that many large cap companies benefiting from these trends are highly profitable. There is also nothing wrong with taking advantage of a market trend or long-term investment theme. However, history shows that the problem occurs when trying to either time the market or making concentrated bets that are inappropriate for one's portfolio. The accompanying chart shows that while technology-related sectors such as Communication Services and Information Technology have outperformed, other sectors have done well this year too. Having too narrow a focus on AI trends, at the expense of overall portfolio diversification, can be problematic for investors as they work toward their long-term goals.

Productivity Is What Drives Long Run Economic Growth

Having a short-term perspective is also problematic because the benefits of past technological innovations were much broader than a few stocks over a year or two. For instance, the benefit of the information technology revolution driven by the rise of personal computers and the growth of internet adoption was not, in hindsight, just concentrated in a few dot-com stocks in the 1990s. Instead, the benefits were broad across industries as all companies adopted new technologies that improved their productivity. In fact, the true impact of these technologies took decades to come to fruition and are still affecting markets today.

Why is productivity so important? In short, productivity allows us to do more with less. This can be difficult to measure and may not always show up in the macroeconomic data the way we expected. When the personal computer and the internet were developed, productivity was relatively stagnant. In the 1980s, the average year-over-year productivity gain was just 1.5%, lower than the previous three decades. Economist Robert Solow called this the "productivity paradox," saying in 1987, “you can see the computer age everywhere but in the productivity statistics.”

Productivity growth finally began accelerating in the early 1990s and remained strong into the early 2000s. This occurred alongside fundamental changes in how businesses delivered products and services. It is difficult to predict how quickly this might occur with AI and how it will transform industries and societies - which is why such predictions are controversial among AI scientists and economists. In a recent paper, MIT economist Daron Acemoglu argues that AI will have its biggest impact if it results in new, higher-value tasks for workers, but that these benefits are not forgone conclusions nor are they likely to be on the scale that some predict.

While recent advancements are impressive, it could take time for AI applications to enhance the productivity of workers. On the one hand, it's possible that we are on the cusp of artificial general intelligence (AGI) - technology that could replace human workers altogether. On the other hand, it's possible that AI will require the right applications and adoption to be valuable. In the meantime, the market will try to gauge what value to place on these possibilities in the stock market. It's important for long-term investors to maintain a broader perspective and not get caught up in the day-to-day hype.

The bottom line? History suggests it's still important to remain diversified amid market exuberance. Doing so allows investors to benefit from recent trends around AI innovations while also positioning their portfolios for long run growth.

- Article posted on 6/13/24 -

Disclaimer

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

This commentary is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Bleakley Financial Group, LLC does not guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Approval #589330

About the Author