Share this article

Consumer spending is the backbone of the U.S. economy, constituting over two-thirds of our nearly $28 trillion GDP. When consumers spend money on everyday goods and services, and make large one-time purchases, it not only helps to spur economic growth but is also a reflection of economic trends. This is because many factors affect consumer purchases including consumer sentiment, the job market, household net worth, inflation, housing prices, the stock market and more. What do investors need to know about the state of the consumer and how it might affect the economy and stock market in the coming year?

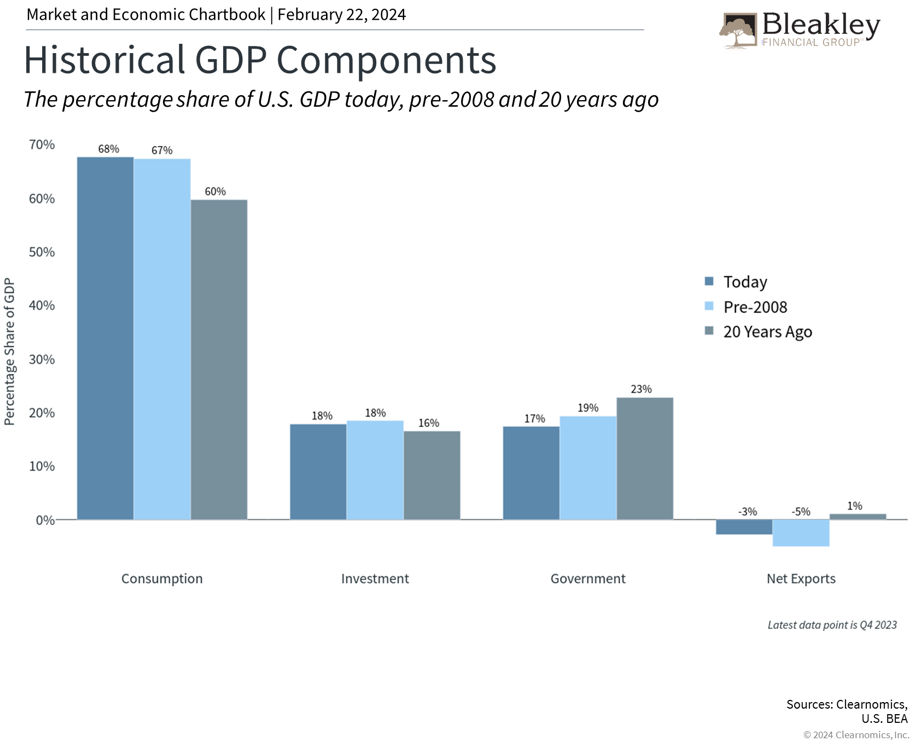

Consumer Spending Is the Largest Component of U.S. GDP

Of the various components of GDP, consumer spending has been the most stable over the past decade at a time when government spending has fluctuated, business investment has been low, and the country has been a net importer of goods. In the fourth quarter of 2023, the economy grew 3.3% with consumer spending contributing 1.9 percentage points to that total. The strength of the consumer has helped the economy stay out of recession despite high inflation rates, layoffs in the tech sector, and ongoing uncertainty. In turn, this has helped to propel the stock market to new all-time highs.

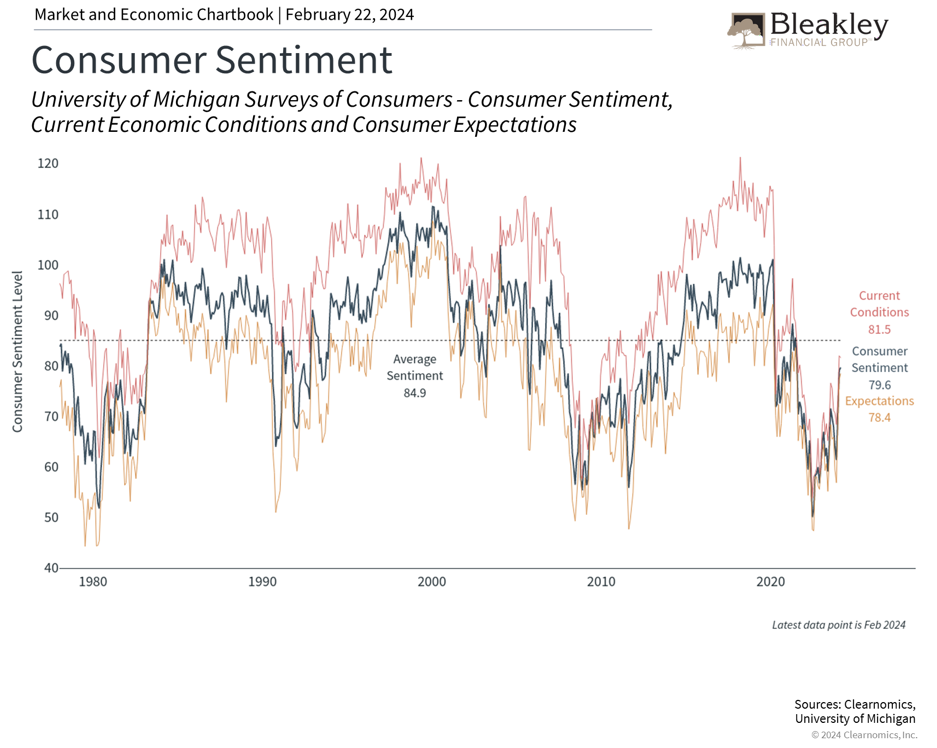

While consumer spending has a direct impact on economic growth, how everyday consumers feel about the economy can vary dramatically over time. Perhaps the best example is the decade following the 2008 global financial crisis. Consumer sentiment was poor for many years due to a weak job market. The housing bust and a sharp decline in manufacturing activity led many to give up on finding work, resulting in a falling labor force participation rate. Even when the overall economy was recovering, consumers were pessimistic. The fact that housing prices collapsed and it took the S&P 500 five years to recover also led to lower consumer net worth.

In many ways, the situation today is the opposite of the post-2008 period. Despite fears of economic weakness, the unemployment rate is still at a historically low 3.7%, 353,000 jobs were added in January, wages have risen over 4% during the past year, and there are still nine million job openings across the country. The fact that the stock market is near all-time highs has also helped to boost the "wealth effect" among consumers. While the housing market still faces many challenges with 30-year mortgage rates around 7%, transactions that do occur are closing at relatively high prices.

Consumers Are Feeling More Optimistic About The Economy

The accompanying chart shows that while consumer sentiment has not yet returned to historical averages after plummeting two years ago, they have improved dramatically. The rise and fall of inflation has been a major contributor to this effect since rising prices directly hit consumer pocketbooks. Inflation rates based on measures such as the Consumer Price Index have improved and the same University of Michigan survey shows that consumers expect inflation over the next year of only 3%. Gasoline prices, for instance, are hovering around $3.20 on average after reaching $5 less than two years ago.

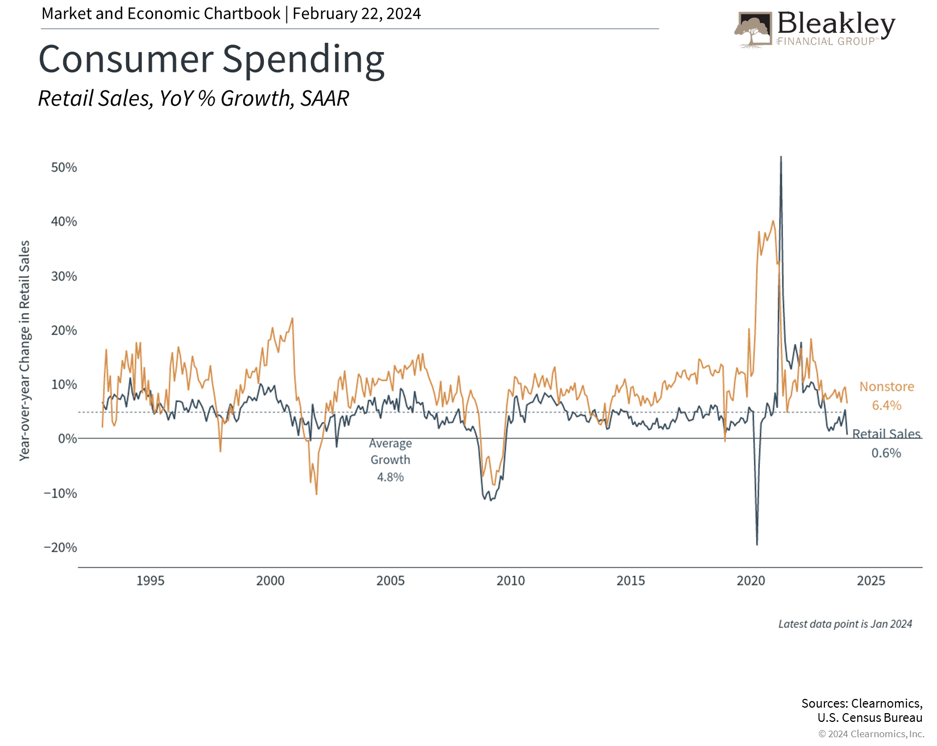

While the consumer story is mostly positive, there are reasons to believe that spending could slow. Households have drawn down their extra cash and savings rates have fallen to only 3.7%, well below the historical average of 6.3%. Recent consumer spending data have also been mixed. On a year-over-year basis, retail sales have decelerated to 0.6%, or -0.8% month-over-month. As the accompanying chart shows, even online retailers have experienced a slowdown in growth after a decade of robust sales growth.

Retail Sales Have Decelerated As Consumers Have Drawn Down Their Savings

Another important piece of the consumer puzzle is the level of household debt. Higher interest rates are a drag on household income statements and balance sheets, especially with the 10-year Treasury yield back around 4.3%. The latest Federal Reserve Bank of New York data show that total credit card debt is just under $1.13 trillion and 9.7% of balances are 90 days delinquent or more. Student loans are also back in the news with the White House seeking to forgive certain eligible borrowers. While there are no easy solutions to these underlying challenges, the financial stress on consumers could improve somewhat as the Fed begins to cut rates later this year.

The bottom line? Consumers are increasingly optimistic as inflation improves and the job market remains strong. While there are still challenges ahead, consumer spending could continue to support the economy and stock market.

- Article posted on 2/26/24 -

Disclaimer

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The market and economic data is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The information in this report has been prepared from data believed to be reliable, but no representation is being made as to its accuracy and completeness.

This commentary is for informational purposes only and is not meant to constitute a recommendation of any particular investment, security, portfolio of securities, transaction or investment strategy. No chart, graph, or other figure provided should be used to determine which securities to buy, sell or hold. No representation is made concerning the appropriateness of any particular investment, security, portfolio of securities, transaction or investment strategy. You should speak with your own financial professional before making any investment decisions.

Past performance is not indicative of future results. Bleakley Financial Group, LLC does not guarantee any specific outcome or profit. These disclosures cannot and do not list every conceivable factor that may affect the results of any investment or investment strategy. Risks will arise, and an investor must be willing and able to accept those risks, including the loss of principal.

Certain statements contained herein are statements of future expectations and other forward looking statements that are based on opinions and assumptions that involve known and unknown risks and uncertainties that would cause actual results, performance or events to differ materially from those expressed or implied in such statements.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings. International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets. The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Approval #545649

About the Author